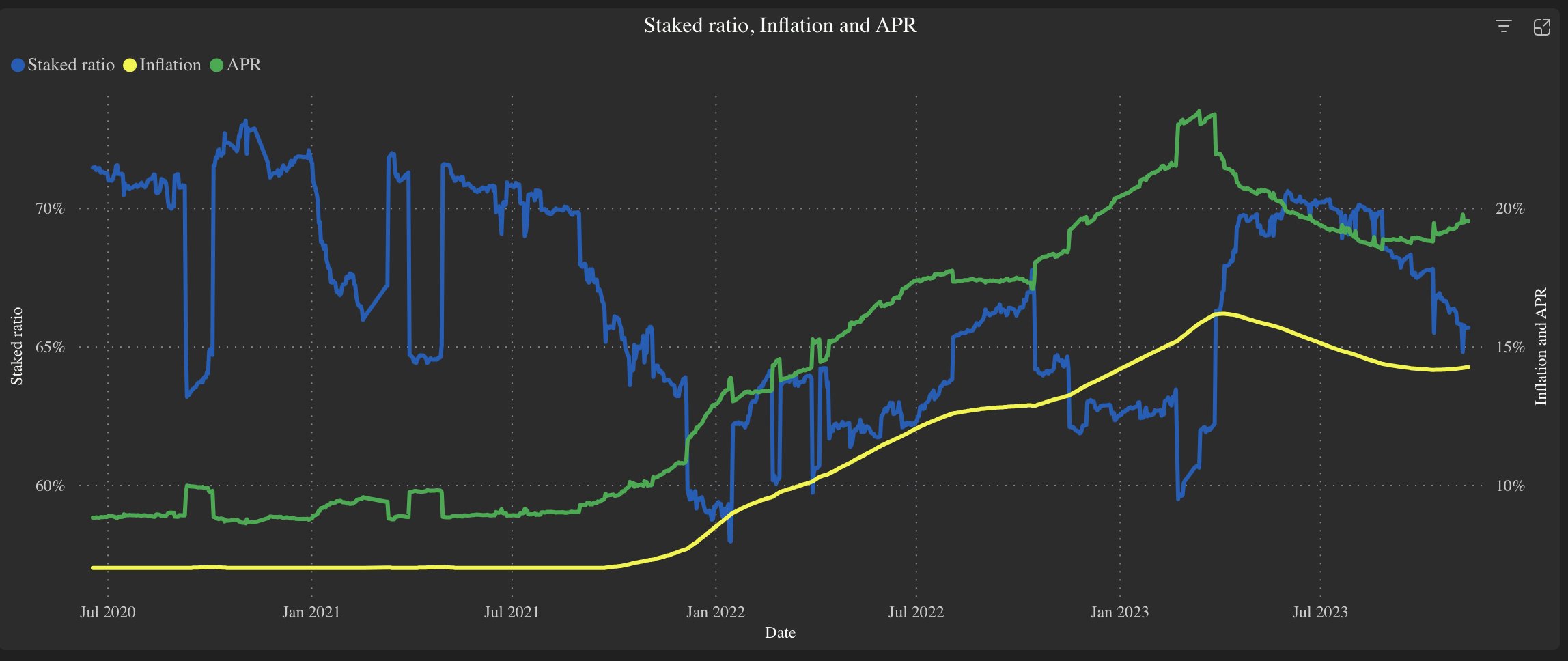

The current inflation is ~14.5% but this is not the max inflation, this is the current balance between 7-20%. If the inflation range is halved to 3.5-10%, then I suppose the inflation wouldn’t be reduced to 10% but to ~7.25% since that would be the balance between 3.5-10%. So this wouldn’t be an already abrupt decreased from ~14.5% to 10%, but lower to around 7%. If the current inflation was 20% because the bonding ratio was low and the inflation range is halved then it would decreased from 20% to 10%, and stay there at the max inflation 10% while staking ratio is low. But given current staking ratio, why would inflation stay at the max new value of 10% if the bonding ratio is around 67%, seems it would stay at the new equilibrium of around 7%, so this would halve the current APR from around 19% to like 9%. It seems this is being sold as max inflation halved from 20% to 10%, but the actual current decrease would just be from ~14.5% to 10%, when actually it would be from 14.5% to around 7%, the new equilibrium in the range 3.5-10%, the new max 10% inflation would happen only with a very low bonding ratio which is not the case currently and very unlikely to happen, as the max 20% had also never happened so far until now.

In the proposal it is written:

‘This proposal seeks to reduce the ATOM inflation rate from ~14% to 10%, which would bring its Staking APR from ~19% to ~13.4%’ → this seems to be highly misleading, because inflation wouldn’t be reduced to 10%, the MAX inflation parameter would be reduced to 10%, but we are currently not at the max inflation of 20% but lower around 14%, so the inflation seems wouldn’t be reduced to 10%, but much lower to the new equilibrium of around 7%

‘Nearly all 180 validators are break-even or profitable at 10% max inflation off of commission alone, and validators have the option to increase their commission rate to help cover operational expenses.’ → this is an absolute lie. Even at the current inflation many validators are at a loss, the costs to run validators is not just the infra costs, there are plenty of other costs involved. Increasing commission is not an option because it leads to losing delegations

The suggestion to reduce inflation was because the price was around $6 and the idea is that by reducing inflation the price would increase. I said before the price is much more related to macro economic factors and BTC price than inflation, and the last 2 weeks just proved what I said: BTC and markets recovered, and without any change to ATOM inflation the price recovered from around $6 to over $9. I understand that for speculating about ATOM price it sounds like a good gamble to try reducing inflation in such an abrupt way, but validators are businesses with fixed and raising costs with more consumer chains so apologies but we are not here to gamble with our revenues. And if your plan doesn’t work and validator revenues are halved without any price increase are you going to compensate and send us these revenues to cover the costs? No, of course you wouldn’t care if many validators go out of business. As @Damien @Vadim_Everstake and many other said, we all agree reducing inflation is good, but this has to be done slowly and considering many factors affecting all stakeholders, not this wild west idea of suddenly deciding to halve inflation and validator revenues. While @jtremback and others have been supporting validators during the bear market with the soft opt-out and other ideas, @zaki_iqlusion has just been saying ‘small validators’ was never a viable business, introducing quietly and without previous discussion a 50% individual validator liquid staking cap limit in the LSM that we had to disable because it was setting the current centralisation of the Cosmos Hub in stone and restricting liquid staking delegations to the smaller validators, and now he is trying to abruptly halve validator revenues in a bear market and with increasing consumer chain costs since Noble will be joining soon as a consumer chain this month likely