@zaki_iqlusion @effortcapital 222 comments and this thread can be easily summarized in ‘halve inflation so that ATOM price does +2x’. If this proposal is approved, and ATOM price doesn’t change or even decreases, because it is much more correlated with BTC price and macro factors than inflation, what is the plan? Will you put another proposal to undo the changes of this proposal?

4 Likes

No, because they think the changes will come in years but they will choose this time of the market cycle to create all the mess. Because they have been here before us and they think they know everything about the cosmos, market, and economics.

They will keep experimenting at the expense of retail investment. I wish everyone knew the actual agenda.

Will the price go up in months and years to come? Yes it will but the prop will have nothing to do with it.

2 Likes

It is ironic that some people, in the low risk and comfort position of a good full time job and with a huge AADAO grant, want to engage in high risk gamblings at the expense of validators, who have been mostly in survival mode since mid 2022. If their employer or AADAO said to them: ok, do this gambling, but if you are wrong in your plan, to align with validators taking the risks, your salary/bonus will be cut at least in half and you will lose half of the AADAO grant. In this case, these people would have thought twice before putting this proposal on-chain. Their employer or the AADAO should have told them similarly as they are telling validators: it is fine, even if your salary, bonus and grant are cut in half or more, no problem you can leave your nice appartment and live in a tent in a park and eat rice every day, you will still be fine don’t worry

3 Likes

All the reasons in the proposal to vote yes are either whimsical or propaganda. Not a single reason to vote yes on this prop but the Cult will make the retail belive that this is in the benefit of retail. The media war of cult is strong. Appriciation for that.

1 Like

Hey Cosmic - the concern of validator sustainability is absolutely valid, and as you know, we have already put out a post related to the Vote Power tax that we think can help with these concerns. I know you like this idea and we absolutely want to bring it to a vote. The plan is to put a signaling proposal up in January and then identify a team that will execute and implement it.

This proposal is not about “halve inflation so price can 2x”, its moreso about making the security budget fall more in-line with the rest of the PoS network market for long term sustainability.

Nobody is lobbying large or small validators to vote “yes” for this proposal. Many small validators are also voting yes for this because they believe its what’s best for the network.

At any point a community member can put up a param change proposal to move it back to 20%. Nobody is stopping that from happening.

1 Like

These are just future promises and there is 0 certainty this proposal will pass, in fact, the probability of the VP tax proposal passing is close to 0. Large validators can be fooled with this inflation halving proposal, fooling them into directly taxing themselves and their delegators will be a more challenging task.

No, it is about halving inflation and hoping for ATOM price to increase by 2x or more. Did you study revenues of validators in other PoS networks so our revenues fall more in-line with their revenues? Because to calculate validator revenues there are several variables such as inflation, bonded ratio, token price, commission. Long term sustainability? I’ve been here before the Cosmos hub genesis launch and so far there is great sustainability after several years.

‘Noboby is lobbying’, that’s why plenty of validators voting no have already been forced to change to abstain or even yes. Careful about this proposal, if it passes, and then ATOM price drops due to some macro events that neither you or nobody can predict, and validators are then even more under water there will be consequences.

Take responsibility at least, if this plan fails and ATOM price doesn’t do 2x as predicted by you or Zaki, take the loss and responsibility and put the proposal to undo this change yourself, what do you say to that?

1 Like

@Cosmic_Validator I know the proposal is called “halving” but in reality inflation will go down from 14% to 10% as such the decline is about -30%. It’s a thirdening. The impact on validators is not as big as you portray. In fact because of this proposal ATOM is up from 6.5 to 9.5 which is a 50% increase which already compensates for the lower rewards. (14 * 6.5 = 91 < 95 = 10 * 9.5)

Can you please stop misrepresenting this proposal. It clearly states that inflation will decline from 14% to 10% in the first paragraph. Any further reward declines depend on bonding ratio targets being met and whether that will happen is speculative. I have every reason to expect big validators to keep gaming the bonding ratio and thus inflation will stay at the upper bound at 10%.

1 Like

The proposal was made based of data that the hub overpays for security.

Your counterpoint is based off what data? Because a 2 minute glance at the charts clearly show ATOM’s price action has largely decoupled from Bitcoin in a negative manner.

2 Likes

I compared the ATOM price to the .BALTMEX index to figure out if the high inflation rate had a negative impact on the ATOM price. I couldnt find evidence that this is the case.

The proposal text is misleading in my opinion since its indicating that the high inflation has “led to constant sell pressure that has hurt its price performance”.

Since we dont want to change the hubs “monetary” policy based on a unfounded claim, we will vote NO on Prop 848

I am sure that if we put the same energy into the community and the AEZ utility as we have put into this topic we will have more success than if we adjust inflation.

By the way, I would be voting NO on a proposal to halve the MIN_INFLATION to 3.5%.

7-10% inflation band is the right level for Cosmos Hub at this stage of its development. I am more concerned with narrowing the possible supply outcomes 10 years out (that is how institutional investors model things) than necessarily driving ATOM inflation into the ground. Going to 4-7% band in 2 or 3 years might makes sense but for the 2024-2025 period 7-10% is fine. Last thing I would want is INCREASING the possible supply outcomes by making the spread between max and min inflation larger from 3% to 6.5%.

I want to see the inflation pegged to 7% for 3 to 6 months in an uninterrupted fashion before considering lowering the min_inflation parameter. I want the market to show me that it wants lower inflation first. At this stage the only thing the market is showing that it wants higher inflation and unfortunately to a degree that erodes the monetary stability of the ATOM token. We have fixed that.

I probably would want to speed up the rate of change so that it doesn’t take forever to go from 10% to 7% if bonding ratio target is met.

I want to address these two posts by Polkachu and Chjango about ATOM’s inflation. It seems that their thinking is influencing some validator votes (which is fine), but I feel like I need to question the merit of some of these arguments:

- Inflation does matter. A lot.

Polkachu says that inflation doesn’t matter, because the overall market cap is all that matters and the inflation is simply a redistribution mechanism from stakers to non-stakers. The relevance of a system in the real world is a function of its accessibility. If you want ATOMs in strong hands all the time, make the inflation 1500% and you will guarantee that the governing stake of the chain remains in the strong hands of the validators over every 3 week period (which is the unstaking period). If your definition of security is the current validators holding the controlling stake, that is what you will do. Inflation is not set at this level because then nobody will use ATOM because it will be inaccessible on exchanges which means its price will be zero. Also it won’t be able to claim that it is “decentralized” or a “public utility” since all the stake is held by a few people. BTW 180 validators is less than 500 investors which is the technical definition of a hedge fund in the US (ie hedge funds can have at most 500 investors). In other words, with the arguments being made here, people are essentially claiming that Cosmos Hub is a hedge fund, not a public utility. A “public” utility is something held by the public (ie more than 500 people). Now the problem is that you have been selling hedge fund shares to the retail investor without registering your securities. I keep repeating this but people don’t seem to understand despite all the people who are going to jail right now. The line between Cosmos Hub heading to jail and not is very thin and it really depends on how decentralized this network is.

Obviously, somebody made a decision to set the max inflation at 20% (Jae has showed his logic on Twitter) and not at 1500% so inflation does indeed matter. The question is whether 20% is the right number.

Even at 20%, there are already validators who are dropping from relaying IBC because the validators are subsidizing IBC. What are the validators subsidizing IBC with? With their own savings that mom and dad gave them? No! With the ATOMs they are awarded. As ATOM price trends towards zero because the fiat monetary aggregates are much tighter than ATOM inflation, the validator’s can’t pay their bills. Here is the problem for the Big Inflation ideologues: you may love staked ATOM, but the price of ATOM is determined by UNSTAKED ATOM trading on exchanges. ATOM’s market cap and link to the rest of the world happens through exchanges which determine its value in fiat. The price of UNSTAKED ATOM is critically important. Validators need fiat to pay the computing cost of those IBC transactions. So if the overall market cap remains the same, but because of very high inflation the price of unstaked ATOM goes towards zero on exchanges, validators will not be able to stay in business and will drop out. They will first drop out of relaying IBC and then they will drop out of validating the Hub.

Cosmos Hub is losing validators because of bad monetary policy. Monetary policy is very important for ANY economic system. That is why you have a Federal Reserve and thousands of PhD economists researching it. Monetary policy has to be fixed so that ATOM price doesn’t trend towards zero and has a monetary value that allows validators to stay in business and validate on the network.

Contrary to what polkachu says - he obviously has never taken a financial class in any capacity - bad tokenomics has wrecked many a shitcoin - just ask Argentina or Zimbabwe. Or Italy. Or Greece. Or Germany. etc. The world is littered with failed tokens (fiat currencies are tokens just like any other). If tokenomics didn’t matter, we would be using sand as payment, but we are not.

-

Changing a parameter is not the same as changing the codebase

Chjango makes equivalency in her post between changing an inflation parameter and a code change that was made to Bitcoin that caused an inflation bug. I don’t know how much of a developer she is and whether she has ever written a line of code, but she clearly can’t distinguish between a configuration change and deployment of new code. No new code is being deployed here. Bugs show up only after new code deployments. Here a configuration change is being made. Many other Cosmos SDK chains change this parameter without any issues. As such there is no technical vulnerability being introduced with this proposal. This is an inappropriate comparison to Bitcoin that verges on deliberate slander to scare other validators into voting NO on the proposal. -

It is absolutely absurd to compare wide sweeping strategic direction initiatives like ATOM 2.0 or technical changes like WASM on the Hub with a simple monetary policy parameter change like this one. These are completely different issues and they don’t go together and shouldn’t be considered together.

-

On some issues, validators interests are most definitely not aligned with their stakers. This is called a “principal-agency” problem - which if the posters had taken any financial certification exam, they would be knowledgeable about. To be posting stuff like MuH VaLidAtOoRs Are Not AliGned wITh UsOoRs is juvenile. You can go be juvenile with your buddies in your backyard, not when you are talking to the world about a $2 billion network.

Thats an awesome way to twist statistics. There are clear 2 camps of yes and no votes. No need to twist it my friend

A public reasoning for a “NO” vote from the Allnodes validator.

Source: https://x.com/allnodes/status/1726222965258551684 (Posted on Nov 19, 2023)

1. Considering Small Validators and Ecosystem Diversity

Low inflation challenges small validators, who already struggle with consumer chain costs. The validator community may become less diverse and more centralized due to budget cuts. The approach ignores tiny validators’ sustainability, which is essential for a decentralized environment.

We’ve come across multiple mentions of Kujira’s “flourishing” environment. However, in the context of Kujira’s low inflation, it’s important to note that running a Kujira validator is not financially viable. Larger validators currently support Kujira by balancing their operations with profits from more profitable chains. However, if all chains adopted a “perfect low inflation” model, even these larger validators may find it unsustainable to continue their services. Ultimately, a system that fails to produce profit is unlikely to remain healthy or sustainable in the long run.

2. Ineffectiveness of Monetary Mechanism in Current Ecosystem Development

Research on cryptocurrencies over the past decade indicates that lowering inflation do not significantly impact token value. Osmosis’ 50% token inflation decrease didn’t change anything. Token’s price didn’t rise. In October 2022 Fantom’s staking rewards were reduced by 60%, in November 2022 the price of FTM was substantially lower. In our opinion it is better to focus on network growth and utility to boost ATOM’s value.

3. Liquid staking derivatives (LSDs) adoption is currently risky

DeFi is great for the Cosmos ecosystem, yet there is also a notable concern about its current state of affairs which resemble a ‘cartel-type’ system, particularly due to Stride’s limited delegation to only 32 validators. The concentrated power in the hands of a few contradicts DeFi’s foundational principles. Consequently, Stride’s current strategy is perceived as a potential threat to the Cosmos ecosystem’s stability and integrity. In this context, the argument that reducing inflation will aid DeFi adoption seems premature and possibly risky given the current state of affairs.

4. Halving vs Current Proposal - A Faulty Parallel

Some people draw the analogy of the Bitcoin halving event with the current proposal. However, Bitcoin halving is an anticipated and well-understood event, allowing for extensive preparation by various stakeholders, such as miners, investors, and traders etc. However, in contrast, what we are dealing with here is an abrupt, short-sighted, and ill-researched idea that might wreak havoc on retail and businesses engaged in building, trading, and validating ATOM.

5. Downward spiral

We sought further insight by consulting a founder of a well-known DEFI Hedge Fund for his perspective on the matter. Here’s his analysis:

Reducing the maximum inflation rate of ATOM from about 14% to 10% would lead to a drop in staking APR by 1/3. This move aims to reduce ATOM’s inflationary nature. However, this could backfire as those who bought ATOM for staking purposes might sell off their tokens, potentially lowering ATOM’s market value.

Furthermore, the decrease in staking yields could make holding ATOM tokens less attractive. With falling yields, a significant number of stakers might withdraw and sell their ATOM, negatively impacting its price. Consequently, even with fewer emissions, ATOM’s value may fall, risking a downward spiral should this proposal be implemented.

6. Summary

Consider the analogy of having a high fever for several days and believing that merely lowering the fever is the cure. So, you take a fever-reducing pill (akin to reducing inflation) to see quick results. You seek support online, and many endorse your approach. Some might even suggest unconventional remedies. You feel optimistic, especially when noticing temporary relief, but this joy is short-lived. A few days later, you are dead because the actual cause of fever was pneumonia.

In other words, the proposal lacks thorough research and demonstrates a significant misunderstanding of various aspects. The author of the idea didn’t even bother himself to reply to people’s questions in his own topic on the cosmos forum while 82.31% (120,780) of all “retail” votes are made from wallets with less than 0.1 ATOM.

It is important to know that we aren’t fundamentally against reducing inflation. But, we advocate for a scientific, predictable, and thoroughly researched approach involving consultations with experts from various fields within the crypto ecosystem and beyond. Any strategy should be meticulously planned well in advance.

Lastly, we feel that the governance system needs some kind of correction. Perhaps introducing barriers such as a higher monetary investment for proposals might be beneficial. Also, an entry exam covering various aspects of the crypto economy, design, and development should be mandatory, ensuring the proposers are qualified and educated.

P.S. What about others who reduced their staking rewards?

I compared pricing of 5 different blockchains between date of halving and date when this topic was created.

Fantom - reduced rewards by 60% (Oct 7, 2022 - Oct 21, 2023)

Event was not planned in advance

Oct 7, 2022: $0.2261

Oct 21, 2023: $0.1825 (-19.28%)

Juno - reduced inflation and rewards by 50% (Oct 25, 2022 - Oct 21, 2023)

Event well planned in advance

Oct 25, 2022: $3.0419

Oct 21, 2023: $0.1402 (-95%)

Osmosis - reduced inflation and rewards by 30% (June 18, 2023 - Oct 21, 2023)

Event well planned in advance

June 18, 2023: $0.5039

Oct 21, 2023: $0.2312 (-55%)

Polygon - reduced rewards by 25% (July 9, 2023 - Oct 21, 2023

Event well planned in advance

July 19, 2022: $0.9614

Oct 21, 2023: $0.5727 (-40%)

Evmos - reduced rewards by 50% (June 1, 2023 - Oct 21, 2023)

Event well planned in advance

June 1: $0.1358

Oct 21: $0.05276 (-61%)

Everyone should make his own conclusions ![]()

2 Likes

This is precisely how its being marketed (read “sold”) on social networks, discords, etc

NWV to Prop 848 – $ATOM Must NOT be Money.

AiB will soon be voting NWV to prop 848, $ATOM “Halving,” which aims at turning the $ATOM token into a monetary token rather than a staking token. We value Cosmos’ core components of security, sustainability, and decentralization, and cannot support a proposal that may threaten its foundational pillars. Halving $ATOM max inflation at this time with insufficient research and discussion will lead to more undesirable outcomes, namely lowering the bonded ratio of staked $ATOMs significantly, hampering the growth of IBC and ICS adoption, affecting the rewards for validators, and placing the entire Cosmos network at risk.

Prop 848 represents a significant shift from the established tokenomics of the Cosmos Hub that has kept our ecosystem secure and dependable since inception. While prop 848 argues that it would enhance the $ATOM Economic Zone (AEZ) and increase $ATOM’s competitiveness in the DeFi space, we disagree categorically and raise the following substantial concerns:

Destabilizing the Security Model

An IBC hub must not be secured by a monetary token. Securing the chain with a monetary token might make sense for non-hubs that don’t rely on the security of its IBC token pegs (for example, if the chain is only concerned about itself). But this isn’t true by definition in the Cosmos of IBC interconnected chains. A good money token is widely distributed by definition, and therefore less by proportion to the whole would be staked to validators. This leaves the governance of the chain open to be taken-over by anyone who has enough of these monetary tokens, and the increase in the liquidity of this token practically guarantees the success of any adversary with sufficient capital. When the competition is the status quo banking system, there is ample capital to be used against the underdog.

In contrast, a staking token that maintains that the supermajority (say ⅔) stays staked has less in circulation as liquid tokens, so the adversary is not guaranteed to be able to purchase enough on the market to succeed in taking over control; while in some cases it may be possible, it is also true that in the scenario with $ATOM as money, the adversary is practically guaranteed success of takeover given reasonable assumptions. It doesn’t make sense in the long run to change what could be secure against the most powerful of adversaries, to one that is guaranteed to fail. And if the reader doesn’t agree that the model should be resilient against the most powerful of adversaries, it means the reader is not aware of history.

Should proposal 848 pass, it starts a precedent of sliding down the slippery slope of degen behavior, encouraging more yield degens to decrease the inflation even further, and in general, the composition and intelligence of the $ATOM token will decrease to such an extent that it will make harmful and dangerous decisions; because the token holders are not experts in tokenomics as they ought to be, and instead only care for short-term yield. This is made worse by the fact that the Gaia Cosmos Hub is an IBC token-pegging hub, and so there will be real incentives for malicious parties to dupe the unsuspecting voters into approving something that is detrimental to the Hub, its users, and Cosmos at large, or for the malicious parties to use its voting power to steal these tokens outright.

$ATOM’s primary utility is – and has always been – staking. $ATOM was never designed to be a monetary token but a staking token enabling an IBC hub that requires the highest level of security (see original token model paper). The original design of $ATOM’s dynamic inflation, acting as a penalty to non-stakers, plays a crucial role in incentivizing network participation and security by intentionally limiting the amount of liquid trading $ATOMs so as to make hostile takeovers prohibitively expensive. Prop 848 risks undermining these foundational principles and destabilizing the network’s security model.

Phantom Revenue and Flawed Arguments

We should not be passing proposals that are based on faulty premises. The way the proponents of prop 848 have been calculating the cost of security, as well as, in general, how the community is calculating staking income or revenue, is fundamentally flawed because $ATOM is a staking token with ⅔ staked. What we need now is to address this problem by better explaining the better mental model to everyone, and by getting the needed clarification from tax authorities. Please note that nothing here is tax advice, and you should talk to your own tax advisors.

When the annual compounded inflation rate of $ATOM is 20%, and because there are generally ⅔ of the $ATOM staked, when you stake your $ATOMs, you earn a 30% return from the original stake, annually. What most people do here is assume that the 30% increase in token supply multiplied by the price of the $ATOM token is all revenue, but we believe this is the wrong way to calculate net revenue for the $ATOM staking token. While the total number of $ATOMs you hold at the end of the year is 1.3x in quantity, the reality is that each $ATOM also went down in proportional utility and value due to the substantial inflation of 20%. What matters is not the number of $ATOMs one holds, but the fraction they hold in comparison to the whole. The effective income considering inflation is actually 1.3x / 1.2x, which equals 8.33%. That is a massive factor of 3.6 to 1.

As a thought exercise, if we were to double the amount of $ATOM tokens every address has, and keep the bonding ratio the same, the price of $ATOM would immediately decrease by 50% (but the net value of our holdings would not change); and usually this shouldn’t be seen as a taxable event, and it isn’t in the case of a stock-split.

As another thought exercise, consider the definition of $MASS = $ATOM / sum($ATOM), where sum($MASS) equals say 1. This unit of measure better represents the intrinsic value of the $ATOM token as a fraction of the whole. With this unit of measure, the calculated income would actually be 8.33% (as opposed to 30% in our example).

Besides the naive model and the $MASS model, the third model says that we should be burning non-staker tokens and claim that the stakers have zero income. This is also reasonable – just because one’s relative ownership in fractions has gone up doesn’t mean that it should be treated as income, since the primary purpose is to disincentivize unbonded tokens and is a form of punishment to a minority subset (of ⅓ more or less). Of course, you can flip this argument around and say that it’s still an incentive for staking (it can be seen as both), so here is a clarifying example; if the $ATOM distribution were like money and massively distributed, and if say only 1% of the $ATOMs were staked, then the inflation going to the stakers is more clearly income.

In comparison, if 99% of the $ATOMs were staked, even with the ludicrous inflation rate of 1,000,000% (for the sake of argument) the inflation shouldn’t be seen as income since the overall distribution by ratio hasn’t changed much at the end of the day; naturally, we perceive this more as a penalty for the 1% that got inflated away. The difference is that the former changes the distribution much more than the latter (generally, the 1% is not like the 100%), and since it depends on a continuous variable (the inflation rate), it is clear that a token can be on a spectrum. Yet it is also correct to say that $ATOM’s original tokenomics makes it primarily a penalty rather than an incentive.

This is not tax advice, but we will approach the relevant tax authorities to get better clarity and argue for this model. Of all the options at our disposal, continuing to calculate revenue/income the naive way is the least favorable, irrational option because it is unnecessarily self-sabotaging.

Those voting in favor of #848 and choosing to deviate from the ⅔ staking target (which is what will happen after #848) are further sabotaging themselves and everyone else by destroying the arguments above in favor of more favorable tax treatment. The inflation rewards of a monetary token are less likely to be seen as a penalty for non-staking, but a positive incentive to stake.

A Bad Precedent

Those who argued in favor of #848 have gone so far as to argue that they are merely gauging the interest of the stakers. This fundamental change to tokenomics that goes counter to security and stability is offered without full disclaimers about the true intended purpose (to make $ATOM a monetary token) and its effects. It is also offered without sufficient planning and guarantees for any sort of consistency, and without the needed disclosures of risks. Indeed we don’t even have a Constitution ratified for the Cosmos Hub yet. Furthermore, to make things worse, this proposal is marketed as a “halvening” which has implications about expected price movements, while what is proposed is nothing at all like the immutable halvening schedule of the Bitcoin chain.

A Further Decline in the Bond Ratio

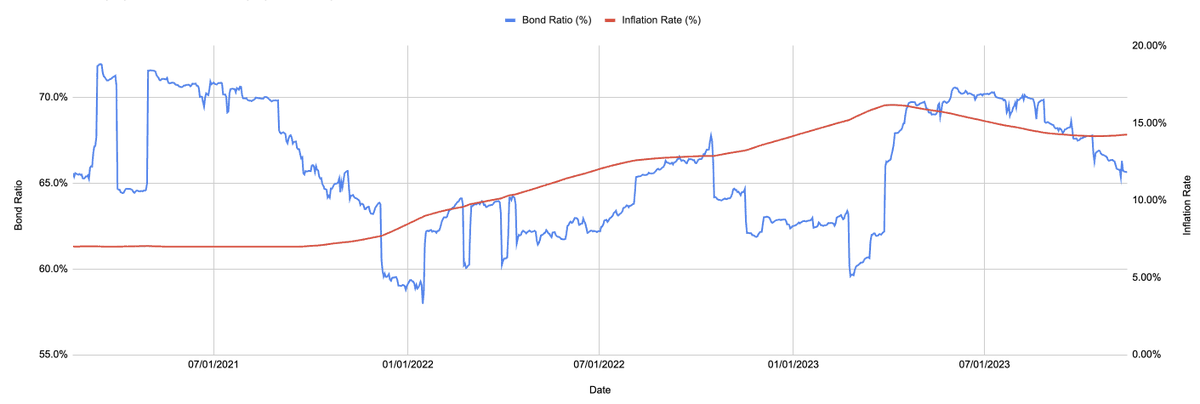

As noted in the proposal, the current bond ratio of the Cosmos Hub is slightly below the target, not surpassing the ⅔ threshold. This existing condition raises a significant concern: by halving the max inflation, the proposal effectively arrests the increase in staking reward rate, a mechanism currently in place to disincentivize non-staking and push the bond ratio towards the target.

The design of the Cosmos network dynamically adjusts the inflation rate to encourage staking when the bond ratio is below the desired threshold. This mechanism is functioning as intended, gradually increasing the inflation rate to incentivize more $ATOM holders to stake their tokens, thereby securing the network. And it has worked as intended in the past, as shown in the graph below. Yet, it was cited as showing that the mechanism doesn’t work using flawed math (however, we concede that the rate of change could be faster). The proposed reduction will likely result in a further decline in the bond ratio when the mechanism should push the ratio to go higher.

The proposal claims that the high $ATOM inflation rate makes DeFi yields less competitive. The proposal states, “However, due to the high inflation rate of $ATOM, DeFi yield can hardly compete which slows down user growth and adoption.” First and foremost this is a gross misunderstanding of the real yield from inflation, which as mentioned before, is with the maximum 20% compounded annual inflation rate, not at most 30% annual yield, but a net 8.33%. Secondly, the reasoning is completely flawed because if the yield from $ATOM is so high then it should increase user growth and adoption, not decrease it. This would be something to celebrate, if true, not stifle.

The higher inflation rate of $ATOM does make it ill-suited for use within DeFi applications because $ATOM inflates more in comparison to the yields. But $ATOM was never intended to be used this way as money. It makes more sense to use a “liquid staking” (a misnomer) service to manage the staking of $ATOM and to use the resulting more deflationary liquid staking tokens within DeFi applications, but compounding rewards like this also compounds the risk and does not come for free.

With the support of such stake management services that offer a more deflationary derivative token, there must be additional checks against hostile takeovers by limiting or throttling how many “liquid staking” tokens can be converted back to $ATOMs. Otherwise, there would be little difference in security between a monetary $ATOM token and a staking $ATOM token, but the distinction between the staking token and the more liquid deflationary token is the basis for introducing control measures with different tradeoffs. Otherwise, we are left with crude levers to manage this key security issue, such as the % of stake that can use ICS, which is not exactly what we need to measure.

IBC Pegged Tokens

The real risk in security here is not with ICS AEZ economics because what is within the AEZ is secured by the same validator set with ICS, and the chain can agree to roll back any transactions that are deemed as leading to theft (e.g. through an exploit). The real risk lies with pegged IBC tokens on the Cosmos Hub. The tokens that are controlled by the Hub but originate from other chains external to the Hub and AEZ are all at risk of being stolen.

All these tokens by default create a real incentive for a malicious actor to exploit. This might be tolerable if the total amount of IBC pegged tokens never exceeded the value of (hypothetically monetary) $ATOM tokens staked divided by 3 (since only ⅓ is guaranteed to be slashable for double-spend attacks with a network partition) but we can’t assume that the Hub will even enforce this invariant when its voters cannot understand the risks of converting $ATOM into a monetary token. Furthermore, most tokens may not be liquid, and re-compensation may not be sufficient recourse for the victims.

Beating the Dead Horse of Validator Incentives

Validator incentives are broken in the Cosmos Hub today. Every validator should be roughly equally incentivized to secure each ICS chain in the AEZ, because the work that every validator should be performing to secure each ICS chain is roughly the same. The current incentive model of rewarding validators in proportion to their stake (multiplied by their set commission) is flawed in this regard because nothing guarantees that tail validators will receive the income they need to remain competitive vs top validators, and this is made worse with ICS scaling. With enough scale, all tail validators will necessarily become insolvent and fail, while the ones that are struggling to stay afloat and survive will necessarily need to make business decisions that affect the security of that validator. This is not only suboptimal but cruel.

The proposed change disproportionately affects smaller validators. While this will cease to be a problem once validator incentives are fixed to be more equal, it still remains a problem until the overall validator incentive model is fixed, and therefore presents an unnecessary risk to smaller validators. One analysis showed that over 74% of Cosmos Hub validators risk becoming unprofitable with less than six consumer chains. Reducing the max inflation can only exacerbate this problem, and make all these validators unprofitable sooner. We should never tolerate the risk of mass validator failures leading to centralization.

The Min Inflation Rate shouldn’t change either

While it is true that with the ICS-enabled transaction scaling, the rewards from transaction fees can and will drive the inflation rate to zero and even negative if we allow it, this is not good if it leads to the promotion and adoption of the $ATOM token as a monetary token (and it will). For this reason, we do not suggest removing the minimum inflation rate bounds of 7% either. This will help retain the intelligence of the $ATOM token distribution and prevent naive token holders from affecting it negatively (and the target demographic of a monetary token is naive because it is the general population).

The negative consequence of keeping the minimum inflation bound at 7% is that the ratio of bonded tokens may rise above ⅔ and the amount of liquid supply may be too small for an accurate measure of the staking token market cap, which can negatively impact the quantifiable security offered by the Hub. However, this effect is limited because when the rewards from ICS transaction throughputs are high (presumably why the bonding rate is high), then there are other ways to calculate the value of the Hub through its continuous revenue, as long as the fees are primarily paid in other tokens besides the $ATOM token.

Where Do We Go From Here?

While we are most staunchly against prop 848 for all the reasons detailed above, there should always be room for experimentation, innovation, and open discussion and debate – as long as we agree to never compromise the network’s security and follow a cautious and measured approach. Given that $ATOM should not be a monetary token, the current design with a minimum inflation rate of 7% and a maximum one of 20% put in place to secure the network is working as intended. Any change to this model would make the $ATOM token too tempting to be marketed as a monetary token.

What we would like to do instead is to open up a discussion for adjusting the NextInflationRate function to become more responsive to reaching the target ratio. Let’s find the best way of doing this together and discuss the pros and cons openly. Balancing market competitiveness with fundamental aspects of network security and economic stability is essential for the continued growth and success of the Cosmos network.

From a bird’s eye perspective looking at the current results of the proposal so far and the discourse we are seeing from the community, there is a clear lack of leadership in guiding the community toward making the necessary decisions. Since proposition 82 we have been working on proposals to improve the governance of the Cosmos Hub that should be prioritized over proposals such as 848. However, the ICF doesn’t appear to be helping and is often involved in backing bad proposals. While we might win here in defeating 848 after we vote NWV (and we urge everyone to do the same, and change votes to NWV), the overall situation is not amenable to what we need in order to succeed, and without active measures, we see this situation continue to worsen.

We will soon publish a plan that will improve this situation with the Hub. Please stay tuned for more information.

3 Likes

Abusing a large bag and influence is detrimental to proper governance. A parameter change isn’t worthy of a veto. Embarrassing conduct.

You can’t say this without precisely explaining what you mean. What type of research ? What type of discussion ? There have been plenty of those in the past couple of months, and really since October 2022 when ATOM 2.0 was proposed (which you voted against with a veto, before proposing an ‘‘Atom One’’ constitution that was heavily rejected, I think I never saw people being as united as when they voted against it.

Odds are you don’t participate in cosmos defi for you to say something so deliberately out of touch, and looking at your address activity that’d be right.

The higher the staking yield is, the higher the defi yields have to be to compete. Nobody will use ATOM as a collateral if it doesn’t pay more than staking. Liquid staking tokens help out solving this, but your founder has repeatedly stated that services like Stride are ‘‘an attack on the hub’’, despite Stride addressing his concerns.

Not with a liquid staked token, which could have been natively implemented with CosmWasm on the Hub, but I guess you vote No With Veto against that too, didn’t you ?

There are many ways to attack a chain like the Hub, and your main fear seems to be about a malicious actor openly buying tokens on the market. I disagree. A lot of the vulnerabilities the Hub had to face (and could have killed it) came from IBC, the concentration of stake to top validators + CEXes and the p2p messaging/mempool.

I think a more realistic and probable angle of attack is a capture of important institutions for the chain, such as yours. AiB used to be an important contributor, and you are now nowhere to be seen except when it comes to dragging those who work for the Hub in the mud.

But I do agree with you that exponentially and indefinitely inflating the supply will detriment anybody from acquiring the token to attack it. Anyway if inflation gets out of control we know what to do, Luna froze its governance when too many tokens were being minted.

If I understand what you are referring to, isn’t this the vision from like 2019 ? I don’t think that’s a fair representation of what the Hub is today.

Alright I’ll stop reading your post here. What am I even looking at.

1 Like

Jae has not proved that 20% is the required inflation to reach 2/3rd staking percentage. This is his own guesstimate. The Cosmos Hub is not the only proof-of-stake chain out there. There are other POS chains with larger market caps that have been researched by advanced academic teams like Cardano (ADA) and Avalanche (AVAX) whose white papers have been written by Prof. Aggelos Kiayias of University of Edinburg and Prof. Emin Gun Sirer of Cornell. I have not seen academic research anywhere that states that 20% inflation rate is needed for 2/3rds bonding ratio. Cardano in particular has made a number of different design choices than ATOM. The ADA token is not bonded for any period of time and is not slashable. These are 2 design decisions that run opposite Jae’s decision to lock up the ATOM token for 21 days and make it slashable. Yet ADA has had more than 2/3rds staked at less than 5% inflation rate since it went into production in 2020. ADA routinely had 70% staked for as long as I have tracked it (which is since 2018). What appear to be disincentives to stake theoretically don’t actually work that way in practice. Cardano to this day has 3 or 4 times the market cap of the Cosmos Hub which means that investors are more comfortable with its security than ATOM’s.

I have taken The Top 20 staking coins from Staking Rewards, all of whom have at least $500 million staked and put their current staking ratios and inflation rates on a chart and ran a polynomial regression line through them. This regression yields the formula you see on the chart. That formula tells me that to achieve 66.67% bonding ratio, the inflation should be 8.76%. In other words, if ATOM has inflation higher than 8.76%, it will achieve its objectives of having at least 2/3rds bonded. If we lower Max Inflation to 10%, we definitely have that ability as such I don’t think the security as Jae defines it (2/3rds bonded) will be impacted in any way.

The entirety of Jae’s argument is that 2/3rds bonding ratio can’t be achieved with 10% inflation and that is an outright false statement because there are 5 chains (ADA, ICP, SEI, EGLD, XTZ) that achieve that level of security with less than 10% inflation. ATOM’s range after this proposal will be from 7% to 10% and that would be higher than 4 out of these 5 coins. XTZ has 4% inflation, EGLD 5.6%, SEI 3.5%, and ADA 2.63%.

Jae’s concerns that the security of the Hub will be affected due to this specific change are entirely speculative.

In addition, I think that “No With Veto” vote is entirely inappropriate here. The proposer has provided his analysis which I find adequate. Prop 848 is a “parameter change” proposal. This is not a wide ranging proposal. This is very specific and well targeted proposal. As such it is not spam. This proposal is very similar to other “parameter change” proposals that were passed with wide majorities recently.

Prop 845 to “increase MaxBlockSize”

Prop 844 to “Update Global Fee Parameters”

Prop 843 to “Increase Global Fee minimum gas prices”.

The Bitcoin Blocksize Wars happened over increasing the block size. Here similar proposal passed with 95% YES vote without much of a discussion or analysis. Nobody was asked to submit detailed analysis. I find Jae’s demands for much deeper analysis on Prop 848 while sleeping through Prop 843-845 a bit arbitrary. Prop 848 does feature far deeper analysis than any of these other parameter change props.

Finally, lowering the Max Inflation rate to 10% does not make ATOM into a monetary token. The new range of 7 to 10% inflation rate is still quite a large penalty for ATOM holders. Currently, Fed rates are at 5% and as such the opportunity cost of holding unstaked ATOM is 5% + 7-10% range or from 12% to 15% per year. No professional investor wants to be holding an asset that is depreciating at the rate of 12% to 15% because they will be fired before 6 months are out. As such there are significant incentinves to stake ATOMs and the concerns for its conversion into a monetary token which will be accumulated for non-staking purposes is very overblown. Even if Fed rates go back down to 0%, ATOM is still losing -7% to -10% per year which is also prohibitive for any professional investors. Investors are there to make money (in fiat), not lose money. If they lose money, they go out of business ![]()

2 Likes

People out here thinking lower inflation = less supply = higher atom price = voting Yes. Other camp saying “lower inflation doesn’t affect price, look at the data”, voting no.

Meanwhile, traders big and small are like “oh, yield is going down, maybe I should move some ATOM to DeFi”. Liquidity goes up, ATOM strategies become reliable, and AEZ-based DeFi protocols start earning revenue.

This prop is not about the supply side y’all.

3 Likes

Validators lack understanding of supply/demand impact to price. They are short term focused given we were in bear market’ survival mode’. Change in inflation for them is considered a haircut on their revenue. Which is true for some period of time. But if you take 1-3y, validators would win massively. But that’s still uncertain in their eyes, why change? Add AiB delegations and we have plenty of No votes.