September 10, 2024

AADAO Oversight Committee Special Report:

Notification Regarding Proposed Bonus Methodology, Alleged Misconduct and/or Mismanagement Involving the General Manager (GM), and Governance Concerns

Table of Contents

I. Executive Summary

II. Background

III. Oversight Decision to Withhold Approval for Proposed Bonus Methodology

IV. Withholding Reasoning

V. 2024 Team Compensation: Salary Base + Retention Bonuses

VI. What Did Cosmos Hub Governance Approve?

VII. Alleged Misconduct and/or Mismanagement Involving the GM

VIII. GM’s Interference with Oversight

IV. GM’s Proposal

X. Conclusion

I. Executive Summary

This communication serves two vital purposes:

- To formally notify the Cosmos Hub community of significant concerns regarding AADAO’s proposed bonus methodology and framework.

- To alert the community to recent events that have substantially compromised the Oversight Committee’s ability to:

a) Perform its duties effectively within AADAO’s established governance structure

b) Exercise reasonable checks and balances

c) Review and investigate alleged misconduct and/or mismanagement involving the General Manager (GM), Youssef Amrani.

These developments have precipitated serious concerns about:

- AADAO’s governance practices

- Financial management and decision-making protocols

- The overall integrity of its executive operations

II. Background

Proposal 865 (AADAO’s renewal mandate), included a provision for the allocation of 100,000 ATOM to be used for a performance and retention-based bonus program. Notably, this proposal passed without clearly defined methodology, Key Performance Indicators (KPIs), and/or assessment frameworks (hereinafter “methodology”) governing the distribution of said bonus ATOM tokens.

The full text of Proposal 865, including supplementary comments, was made available via an IPFS pin. The pertinent section of the full text states verbatim:

“AADAO plans to distribute up to 100,000 ATOMs across its team as part of an ATOM Alignment Allocation. This allocation plan is multi-dimensional, focusing on performance and retention of key talent and is described here. The bonuses are neither automatic nor guaranteed, and are subject to review of the Strategy Committee and Oversight.”

“AADAO Performance and Retention Bonus Protocol.”

The above document was NOT incorporated as a direct link within the on-chain version of the proposal text; its accessibility was limited to a hyperlink within the IPFS pin and the Cosmos Hub Forum post for Proposal 865.

The protocol document delineates the distribution of the bonus pool as follows:

The 100,000 bonus ATOM is allocated with a 90% cap:

- Performance Bonuses: up to 70% of the total ATOM bonus pool (70,000 ATOM).

- Retention Bonuses: up to 20% of the total ATOM bonus pool (20,000 ATOM, with distribution commencing February 2024).

- Strategic Bonuses (team-base performance bonus for Strategy Committee members): 10% of the total ATOM bonus pool (10,000 ATOM)

The document further outlines the grading methodology for performance-based bonuses as follows:

- "Below Expectations" (0% of maximum allocation): The team or contributor fails to meet their commitments and KPIs. Ineligible for performance bonus.

- "Meets Expectations" (50% of maximum allocation): The team or contributor fulfills their commitments and meets KPIs. Eligible for middle tier performance bonus.

- "Above Expectations" (100% of maximum allocation): The team or contributor exceeds their commitments and surpasses KPIs. Eligible for up to the allocated maximum bonus.

While the proposed methodology broadly adheres to the rudimentary plan described in the referenced document, Oversight contends the lack of visibility and attention given to this document means it cannot be assumed to be “ratified” scope as per 865. In fact, several validators who voted Yes to 865, do not recall ever seeing the Bonus Protocol document.

Subsequent to the ratification of 865, there have been material delays in the formalization of the methodology to be used for the distribution of bonus ATOM to individual contributors and subDAO teams.

The GM assumed primary responsibility for the research and development of said methodology. The Strategy Committee, comprising of Mark D, “Better Future”/Ryan Orr, and Carter Woetzel, approved the methodology before it was conveyed to Oversight for final approval and implementation.

Currently, the Oversight Committee consists of the Financial Controller/Accountant (Patricia Mizuki) and the Elected Member (Grace Yu). The Oversight Coordinator position is currently vacant due to Damien Bonello’s departure in May, and in the interim, Grace has assumed several of the Coordinator’s responsibilities.

The Oversight Committee’s mandate in the bonus process is twofold:

- Approve the proposed bonus methodology and related KPIs (individual, team)

- Ensure transparent communication of both the methodology and germane information to the Cosmos Hub community

III. Decision to Withhold Approval for Proposed Bonus Methodology

After thorough review and deliberation, Oversight decided to withhold approval for the proposed bonus methodology. The Oversight members communicated this decision to the core DAO contributors on August 29th.

Had this methodology been sanctioned by Oversight, it would have initiated the vesting of ATOM from the bonus pool for individual performance-based bonuses commencing September 1, 2024.

IV. Withholding Reasoning

The primary rationale for withholding arises from what we deem to be an inappropriate application and utilization of the bonus program to establish what we perceive as variable compensation mechanisms influencing total potential compensation.

It is the position of the Oversight Committee that bonus ATOM should be exclusively reserved for performance that “exceeds expectations” or is deemed exceptional.

Furthermore, we maintain that the manner in which AADAO communicated its intended use of bonus ATOM during the pre-proposal phase and voting period of Proposal 865 strongly implied that the bonus pool would be utilized to incentivize measurable excellence.

The GM contends that the proposed utilization of ATOM bonuses for performance that “meets expectations” was ratified by governance because the Bonus Performance and Retention Protocol was shared. He also argued that rewarding performance meeting baseline expectations aligns with “industry standards”, we respectfully dispute this interpretation. There’s considerable variation as to how bonuses are used within a given industry depending on stage of business, and nature of the job being done.

We also find it problematic that select contributors of the DAO, particularly the GM, did not want to disclose the individual performance-based KPIs to the community for validation before proceeding with implementation.

Oversight asserts that the bonus pool should not be misused to “reward” unexceptional performance that merely “meets expectations”. Additionally, given the current price action of ATOM, the proposed methodology is all the more indefensible.

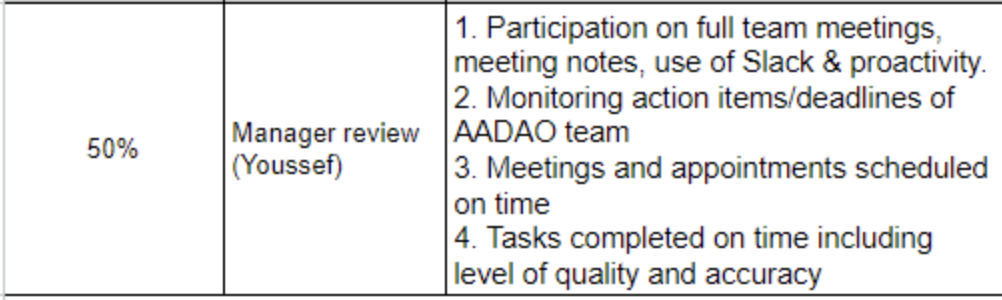

To illustrate our misgivings with the proposed methodology, consider the following example of KPIs used for "meets expectations"under which a contributor would be eligible to receive 50% of their performance-based ATOM allocation (with Youssef Amrani, GM, serving as the direct report):

Oversight also disapproves of AADAO’s recruiting practice of guaranteeing the disbursement of bonus ATOM for “average performance” in inducing potential contributors to accept relatively under-market base salaries.

(Sarah Braxenhall and Erin Vanderberg were prospective leads for the Marketing and BD SubDAOs)

Additional reasons for withholding approval:

- Disproportionate favoring of senior roles within the proposed bonus methodology –with the applied methodology lacking parity, equitability and consistency.

- Potential perpetuation of compensation disparities existing between the GM and the rest of the contributor team.

- Ineffective incentivization scheme for contributor excellence; bonus ATOM is utilized for performance that “meets expectations” rather than “exceeds expectations”.

- Individual KPIs lack objectivity and “SMART” attributes: specific, measurable, actionable/achievable, relevant, time-bound.

- COIs in assigning the GM’s bonus assessment to StratComm members (vulnerable to quid pro quo)

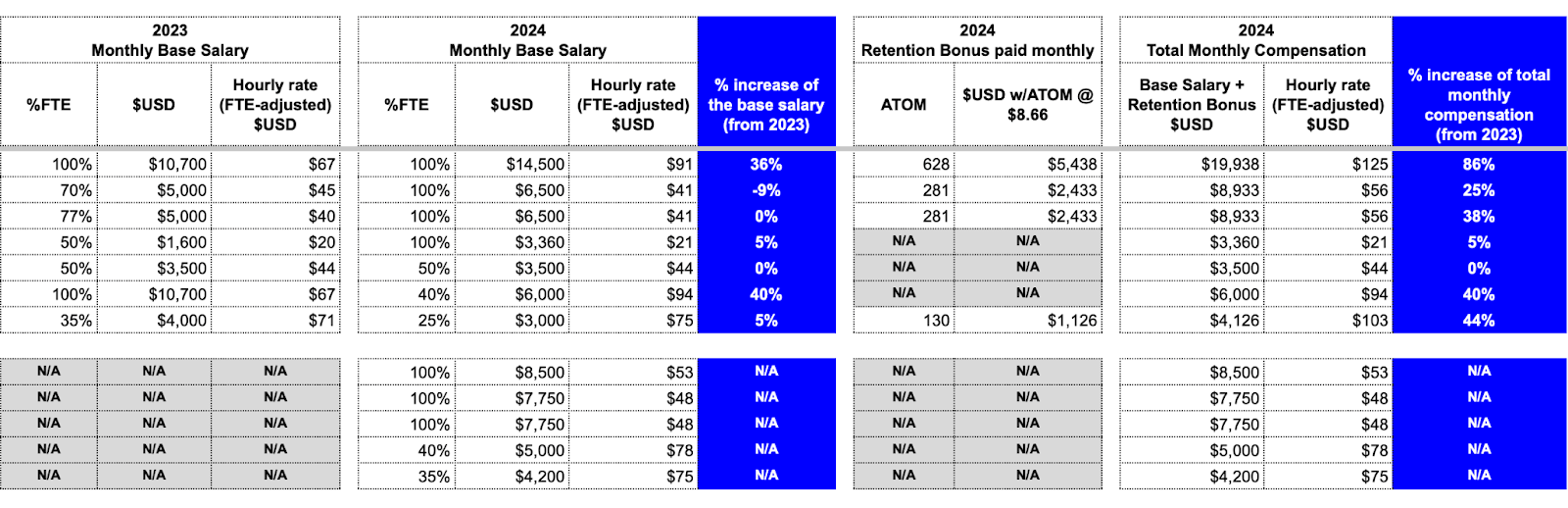

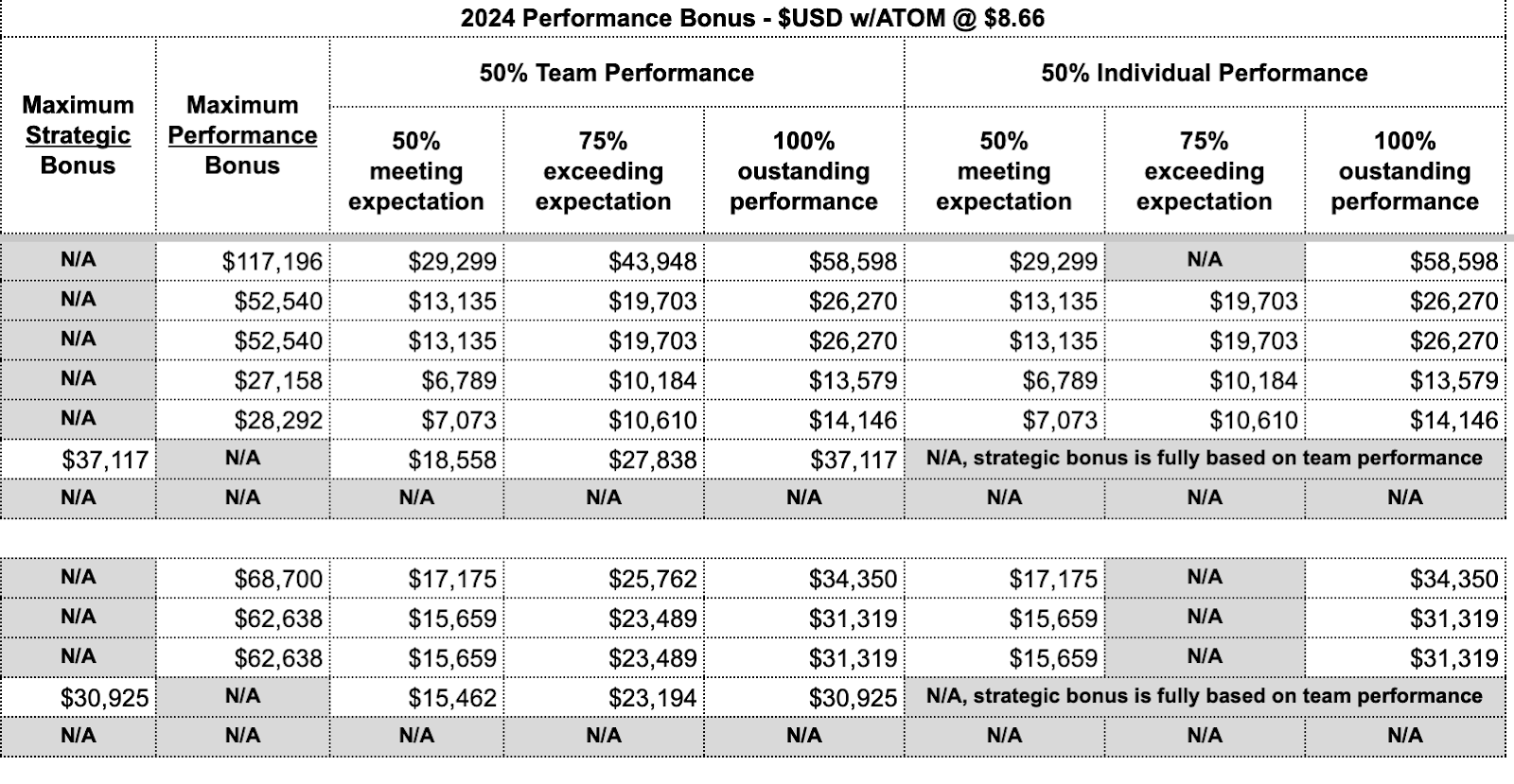

V. 2024 Team Compensation: Salary Base + Retention Bonuses

The distribution formula for various bonus categories—including retention bonuses, performance-based bonuses (both individual and team), and performance-based bonuses specifically for Strategy Committee members—all employ 2024 base salaries as the foundational metric for determining maximum ATOM allocation amounts.

Such an approach may inadvertently amplify pre-existing compensation inequities within the organization’s remuneration structure.

This issue is particularly problematic given that many contributors, especially recent hires, have accepted sub-market base salaries and are not recipients of “retention bonuses”.

In the interest of transparency, we deem it necessary to show you how AADAO “compensation brackets” translate into base annual salaries, and to disclose what eligible contributors have been receiving since February 2024 in the form of monthly “retention bonuses”, affecting total monthly comp.

As noted earlier, please remember that the retention bonus utilize 20% of the 100,000 ATOM bonus pool and allocated using a pro rata rate of 2024 base salaries.

It is important to highlight that the performance bonuses (team, individual, strategy) have not yet been distributed. This delay is due to objections raised by Oversight regarding the potential for these bonuses to further exacerbate compensation disparities if implemented as proposed.

Please note, the Financial Controller has determined that utilizing the daily average ATOM price from Jan 1 - Aug 24, 2024, represents the most appropriate and accurate method for estimating the USD value of the ATOM retention bonus. $8.66 US is the daily ATOM average for the referenced time period.

The primary calculation of ATOM value of $8.66 USD has been used for all relevant computations within this spreadsheet: AADAO Historic Team Compensation & Bonus Distribution (prepared by AADAO Oversight).

AADAO Published Compensation Brackets: (per Proposal 865)

- Program Manager and Strategy Committee Members: $75 - $95 per hour

- Technical/Developer Member: $45 - $65 per hour

- Reviewer Committee Member: $35 - $55 per hour

- Administrative Member: $15 - $20 per hour

In view of the above concerns, Oversight has recommended a comprehensive review of the proposed methodology to effect a policy that reflects greater parity with improved KPIs and incentives across the organization.

We have also instructed the DAO to communicate its use of the ATOM bonus pool with clear and precise terminology that accurately describes how the ATOM is being used. If it’s not being used as a “bonus” consistent with community’s association of bonuses with exceptional performance, it should not be described as a bonus methodology.

While it can be argued that compensation structures and agreements fall outside the purview of Oversight, we contend that our involvement is warranted and necessary in this case. Compensation structures and bonus schemas are fundamentally a resource utilization question. If ATOM is being used inconsistently or inequitably, it is within our core responsibilities and public obligation to question why contributor salaries remain relatively non-competitive while the GM’s salary is maintained at “market-competitive” levels.

We believe how salary bands interact with bonus mechanics fall within the scope of oversight review, especially if it yields outcomes that lack a fair distribution of ATOM incentives.

VI. What Did Cosmos Hub Governance Approve?

AADAO’s GM contends that his approach to using the ATOM bonus pool was “ratified” by the “sovereign voice” of Cosmos Hub governance through the passage of Proposal 865. Oversight believes he is conflating the Governance provision of 100,000 ATOM with the methodology used to distribute it. These are not the same things. Especially given that a meaningful methodology and its relevant KPIs were not shared with stakeholders during the voting period.

The GM’s insistence that the use of bonuses for “meets expectations” raises material questions regarding the scope of voter approval.

Given these divergent perspectives, the Oversight Committee urgently seeks clarity from the community regarding your understanding of what was ratified with respect to AADAO bonuses in Proposal 865.

Specifically:

-

Did you interpret a “YES” vote on Proposal 865 as constituting approval of all policies within the linked documents, e.g., the “AADAO Performance and Retention Bonus Protocol”?

-

In your opinion, does the passage of a proposal implicitly ratify all linked documents and their contents, or should such ratifications be more explicit? Furthermore, how is the sufficiency of document linkage determined, and where should such links be presented?

-

Was it explicitly clear that the 100,000 ATOM bonus allocation for “Performance and Retention” could be utilized as compensation tools supplementing monthly salaries?

-

Is it appropriate to use the bonus pool for contributor performance that “meets expectations” or must it be used for performance that “exceeds expectations”, only or more?

Your insights on these matters are essential. We ask for your opinions on the above, in this Forum by Monday, September 23rd.

VII. Alleged Misconduct and/or Mismanagement Involving the GM, Youssef Amrani

On August 30, 2024, six out of nine contributors convened for the weekly scheduled Strategy Committee call. The exclusive objective of this call was to have the GM’s rationale for the proposed bonus methodology, and to ascertain the extent of Strategy Committee members’ awareness regarding the bonus methodology’s impact on the total compensation of all contributors.

During this meeting, the GM was asked to provide justification for the competitive nature of his base salary in contrast to the sub-market compensation of other contributors, and to explain the apparent disproportionate allocation of bonuses in his favor.

In the course of this call, the GM alleged that the Financial Controller had been withholding approval of the proposed methodology due to the GM’s refusal to accede to her purported request for performance-based bonuses. The GM further alleged that the Controller’s withholding of approval was retaliatory in nature and that she was “lacking integrity.”

In response to these allegations, the Controller provided a rebuttal, asserting that the GM’s claim regarding her request for performance-based bonuses is a misrepresentation of their prior discussions.

The Controller explained that she had, in fact, argued that the lack of objectivity in the GM’s proposed KPIs would theoretically qualify Oversight members to receive performance-based bonuses, a point she had raised to illustrate the perceived inefficacy of the GM’s suggested KPIs. The Controller affirmed that she had previously explained to the GM that Oversight’s function, not directly accruing value to ATOM, should preclude it from eligibility for performance-based ATOM bonuses.

The Controller further explained the origin of her professional disagreements with the GM, tracing them to February 2024. At that time, the GM had shared a document, expressly designated as “confidential,” exclusively with the Controller. This document revealed the effect of retention bonuses on monthly compensation rates.

Upon receipt and review of this document, the Controller averred that she perceived the GM’s total possible compensation as being worrisome. In accordance with her fiduciary duties, she subsequently consulted the then-Oversight Coordinator regarding her concerns. Following deliberations, both Oversight members concurred that the GM’s salary appeared to be excessive and potentially “abusive.”

In light of these concerns, the Oversight members agreed that it would be prudent to raise questions regarding the retention methodology proposed by the GM. Specifically, they questioned the GM’s insistence on utilizing 2024 base salaries for the retention formula, asserting that this approach compounded what they perceived as a double dip benefit for the GM.

In comparison to the 2023 base salary structure, all returning contributors had accepted reduced base salaries, with a mere two out of seven receiving a nominal 5% raise in base salary. In stark contrast, the GM gave himself a 36% raise to his own base salary. Because the GM’s retention-based formula utilizes 2024 salaries, as opposed to 2023 salaries, this results in yielding an 86% increase (assuming an ATOM average value of $8.66) for the GM’s 2024 total monthly compensation, when compared to his monthly remuneration during the 2023 pilot year.

Furthermore, this retention formula makes the GM the beneficiary of 50% of all available retention-based ATOM. The obvious gaps in compensation and proposed bonus allocation illustrates the obvious conflicts of interest involved when the GM has singular discretion in negotiating compensation, and designing the bonus structures.

The Controller attested that she had conducted research and consulted with professionals regarding standard practices for retention formula calculations, subsequently communicating to the GM that the normative practice is to reference 2023 base salaries rather than 2024 base salaries. The Controller reported that the GM responded with hostility to this suggestion. Furthermore, the Controller alleged that subsequent to her conversation with the GM on this matter, she received a phone call from the GM’s spouse, which she described as aggressive, verbally abusive, and intimidating in nature.

Despite the recommendations from the Controller and the former Oversight Coordinator to utilize 2023 base salaries for the retention bonus calculation, the GM unilaterally implemented the use of his preferred formula.

The Controller reported that subsequent to these challenges, she experienced additional confrontations with the GM as he developed and proposed the “final KPIs” for individual performance-based bonuses. The Controller consistently argued that these KPIs lacked objectivity and specificity.

The Controller alleged that the GM frequently resorted to a pattern of diminishment, with her “integrity” being impugned whenever she exercised or expressed reasonable criticism against the GM’s various ideas. She reported being routinely accused of “over-reaching” and alleged that she had been threatened with removal if she did not acquiesce to and comply with the GM’s directives.

Areas of Potential Misconduct and Mismanagement:

These points outline the material issues of potential violations in behavior and business practices, if the Financial Controller’s provided testimony is true.

A. Abuse of Compensation Structures:

- Excessive and potentially “abusive” compensation practices

- Lack of transparency and disclosure regarding total monthly compensation

- Excessive 86% increase in the GM’s base salary from the previous fiscal year

- Improper utilization of retention bonuses to inflate monthly compensation

- Absence of proper oversight and controls on determinations of total compensation and bonus schemes

B. Interference with Oversight Functions:

- Alleged obstruction of oversight duties

- Potential intimidation and coercion of oversight committee members

- Undue influence on oversight processes and decision-making

- Manipulation of oversight personnel to suppress inquiries and concerns

C. Inappropriate External Interference:

- Unauthorized involvement of non-DAO personnel in internal financial, accounting, and governance matters

- Improper influence exerted by external individuals on internal DAO operations

- Violation of professional boundaries and disregard for COIs and internal controls

D. Creation of a Hostile Work Environment:

- Alleged verbal abuse and intimidation of oversight personnel

- Retaliatory threats against Oversight members performing diligence

- Suppression of legitimate inquiries through aggressive verbal threats and retaliatory behavior

E. Fiduciary Duty and Lack of Transparency:

- Willful withholding of pertinent financial information from oversight and other core DAO members

- Resistance to legitimate inquiries regarding compensation, retention, and bonus related methodologies

- Directing obfuscation of financial data to evade scrutiny (Controller was directed to disburse performance-based ATOM bonus monthly to deter attention from the community)

F. Subversion of Oversight Mechanisms:

- Potential rendering of oversight functions as merely perfunctory

- Manipulation and compromise of established oversight processes

- Breach of fair governance principles and internal control mechanisms

G. Conflicts of Interest:

- Singular and unchecked discretion and control in defining and distributing bonus allocations affecting himself and other contributors

- Lack of sufficient checks and balances in compensation related decision-making processes

- Potential self-dealing in the determination of one’s own compensation and bonus benefits

- Unauthorized and inappropriate involvement of spouse in DAO financial matters, creating a conflict between personal and organizational interests

- Alleged use of retention bonuses to disproportionately benefit self, potentially at the expense of other contributors’ possible total compensation

- Alleged pressure on oversight members to approve financial methodologies that disproportionately benefit self

- Potential misuse of DAO resources and/or role for personal benefit

- Alleged creation of a governance structure that centralizes power and decision-making authority; potentially compromising organizational checks and balances

VIII. GM’s Interference with Oversight’s Function

In light of the serious allegations involving both the GM and the Financial Controller, the Elected Member, in the aftermath of the August 30th call, prepared an Incident Report to memorialize the allegations and concerns expressed.

The report explicitly stated its purpose as serving as a formal record of the concerns raised and to notify the contributor team of the initiation of a review process. The report emphasized that no definitive conclusions had been drawn, pending further review and corroboration of the concerns and allegations.

On September 2nd, the Elected Member shared a structural framework for the review/investigation process. This action was explained as the Oversight Committee’s fiduciary duty to ensure proper governance and to address the serious allegations of misconduct and potential breaches of organizational policies.

On September 2nd, the Elected Member shared structure and process regarding her initiated review into the allegations of misconduct and/or mismanagement with all core contributors, transparently.

On a September 4th call with Strategy Committee members, she explained that the purpose of the review was for internal purposes, intended to inform corrective and remedial actions addressing any validated issues of misconduct or governance and or operational deficiencies. At the conclusion of this call, it is true to say all the Strategy Committee members and core contributors to the DAO had acknowledged acceptance of, and agreement with the Elected Member’s process. There are no existing protocols that establish how reviews and or investigations of misconduct are to be executed – therefore, the Elected Member is developing a process where one does not exist.

The review had been proceeding with team-wide agreement.

On September 5th, the GM shared a “Communique” addressed to the Elected Member ordering her to “cease and desist” her review.

Since August 30th, the GM has been actively avoidant, and it has not been possible for the Elected Member to schedule an interview to ascertain his account of events relating to concerns of his misconduct. Prior to the GM’s demand for the Elected Member to suspend the the review, preliminary findings from the investigation indicate:

-

The material issues described in an internal Incident Report shared with core DAO members on August 30th, appear to be substantiated in meaningful part, if not in full.

-

This assessment is based on:

- Interviews conducted with relevant parties (names will be withheld for confidentiality concerns)

- Review of pertinent documentation

- Examination of communication records related to the alleged misconduct/mismanagement

Oversight views the GM’s “cease and desist” demand to be unreasonable and demonstrative of the alleged intimidation and bullying behavior the Financial Controller has endured throughout the current fiscal year.

IX. The GM’s Proposal

The GM has levied allegations against the Elected Member, asserting that she has committed a breach of confidentiality and violated professional ethical practices by sharing the Incident Report with core contributors. Furthermore, the GM contends that the Elected Member is incapacitated from conducting the review due to what he alleges to be her “bias” and/or partiality, thereby compromising her ability to maintain objectivity in the investigative process.

In light of these allegations, the GM has proposed the engagement of an independent investigator or an ombudsman-like figure to adjudicate the issues pertaining to his alleged misconduct and mismanagement.

The financial implications of the GM’s proposal are both substantial and ambiguous. It is noteworthy that the engagement of an ombudsman is not a trivial undertaking from a cost perspective. In a communication via the Slack platform, the GM indicated that he is “happy to contribute” with reference to his proposal; however, the extent and nature of this purported contribution remain unclear.

The Elected Member has, on multiple occasions, sought clarification from the GM as to whether his contribution is economic in nature. To date, these inquiries have gone unanswered.

Potential Use of DAO Resources

If the GM’s proposed external investigation necessitates the utilization of DAO resources, it is the unequivocal position of the Oversight Committee that the community must be apprised of this potential resource allocation.

In principle, Oversight is not inherently opposed to the engagement of an ombudsman. However, the GM’s proposal to retain an external investigator or ombudsman engenders several substantive concerns:

-

The financial implications of such an engagement are both substantial and lacking in clarity. While the GM has expressed that he is “happy to contribute,” the extent and nature of this putative contribution are unknown.

-

Should this proposal involve the use of DAO resources, it would constitute a significant expenditure outside the purview of funded key activities, potentially contravening the understanding of how DAO resources are to be used as per Proposal 865.

-

GM’s proposal presents a clear and material conflict of interest. It appears to be an attempt to utilize DAO resources to circumvent or undermine the proximate and established oversight mechanisms. It is imperative to note that the Oversight Committee is constituted with the express mandate to perform checks and balances within the organizational structure.

-

The proposal bears the hallmarks of an obstruction tactic, potentially representing an injudicious use of public resources for a measure that serves the GM’s personal interests rather than those of the AADAO team or the broader community.

These concerns collectively underscore the need for careful consideration and community consultation before any action is taken on the GM’s proposal.

X. Conclusion

While Patricia and I acknowledge that the issues delineated herein may elicit strong emotional responses, we earnestly urge the community to exercise restraint in forming premature judgments.

The Oversight Committee wishes to emphasize, that the conduct of the General Manager should not be construed as reflective of other core contributors’ integrity or performance.

It aggrieves us to make this report - mainly because unlike the GM, Youssef Amrani, we are not naive to the undesirable and undeserved negative effects his actions can have for the AADAO collective. It is our observation that many core contributors are diligent, impassioned, and upright persons who duly understand and embrace their organizational identity as a Cosmos Hub community owned DAO.

Several of the contributors explicitly communicated to Oversight, they do not believe a bonus methodology is tenable or defensible given the current ATOM climate. It is fair to say, the methodology was persistently pushed, and had escalated to this level of team-wide consideration because the GM desires to see it implemented with urgency.

Therefore, we deem it necessary to caution against precipitous or premature calls for the dissolution or termination of AADAO, as such actions would be unwarranted at this juncture.

Instead, we respectfully submit that the community’s discourse should, at present, be circumscribed to addressing the specific inquiries posed in Section V of this report.

Additionally, we solicit the community’s considered opinion on the propriety of the GM’s proposal to engage an external investigator/ombudsman, and whether the community sanctions such an expenditure.

The Oversight Committee reaffirms its unwavering commitment to ensuring transparency, accountability, and the proper utilization of Hub community resources. We express our profound appreciation for your ongoing engagement and solicit your necessary support in understanding and addressing these critical governance matters.

Respectfully submitted,

Grace

Elected Member, AADAO Oversight Committee

Patricia @Patricia

Financial Controller, AADAO Oversight Committee

References

AADAO Compensation & Bonuses:

- Proposal 865, Mintscan

- Proposal 865, Cosmos Hub Forum

- AADAO Next Steps, Cosmos Hub Forum

- IPFS Pin – Full Text with Comments (Proposal 865)

- AADAO Performance Bonus Structure (this document was not linked in the text of Proposal 865, rather it was linked to the IPFS pin and shared on Forum)

- Transparency Report 7 (please see “Performance Bonus”)

- AADAO Historic Compensation (2023 & 2024) and Bonus Distribution